What is Universal Life Insurance?

A universal life insurance policy is a mixture of a permanent life insurance policy and an investment account. So why not just get a term policy, and invest on your own? Good question.

Here are a few reasons why people opt for an IUL policy instead of buying a term life policy, and investing on their own:

- The life insurance policy covers you for life. No deadline to worry about.

- The cost never increases, and the coverage only increases.

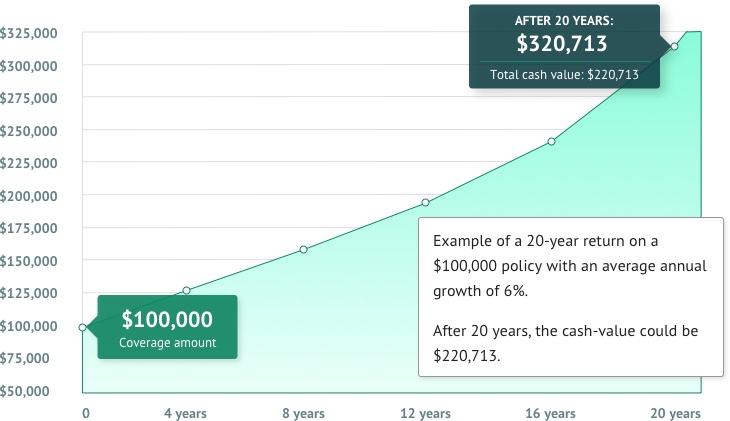

- The cash value an IUL policy builds is entirely tax-free.

- Some policies provide caps and floors on your investment. While this means your max return is limited to say, 9%, it also means that your max loss may be limited to 0%.

- You can choose between various investment types, like the S&P 500. Or you can opt for managed investments instead.

- An excellent choice for tax-free death benefits, after other options have been exchausted, such as 401(k)s and IRAs.

Is universal life insurance a good fit for me?

People of all ages buy universal life insurance, but it's most popular for individuals mid 30's and older. A universal life insurance policy allows you to combine the convenience of permanent life insurance with a tax-free investment account, without much of the hassle.

It may take a few years before the policy actually starts to accumulate interest, but once it does, it accumulates year after year. This allows for long-term growth of wealth.

Best Universal Life Insurance Companies

Cash value sounds great, but how can I use it?

Retirement

Imagine being able to supplement your retirement with a life insurance policy you bought 20-30 years ago. It's one of the biggest reasons opt for universal life insurance.

Paying off loans

One of the biggest costs in our lives are loans. The interest we pay typically far exceeds the gain of any sort of investment. You can use the built up cash value to pay off your vehicle, your home, or other loans.

Increasing the death benefit

If there's no need for you to access the built up cash-value, you can simply leave it alone. Once you pass away, any built up cash value will be added to your death benefit and paid to your beneficiaries.

The different types of Universal Life insurance

Universal life insurance comes in a few different types, with important differences.

Traditional Universal Life

These policies generally accumulate cash value more slowly than the other types do but they’re also safer, as the cash value accumulates in money market accounts. Many people use this type of policy to supplement their retirement income needs by taking loans against the policy after retirement.

Pros

- Money market accounts are generally a safe investment.

- No need to stress or worry about your investment.

Indexed Universal Life

Indexed life insurance policies policies are invested in index funds that usually follow the S&P 500 or a similar equity index. Many of the features and options of an indexed policy mimic those of a traditional policy; the biggest difference is that the gains are usually larger. These policies are usually used to augment other investment options in a long-term strategy, combining protection with growth of wealth.

Pros

- A healthy mix between risk and cash value growth.

- Typically used for long-term growth of wealth.

- For safer investments, some carriers offer a floor and cap to minimize risk.

Cons

- In a bear market, your investment could lose money. Or if a floor is in place, it could simply not grow cash-value.

Variable Universal Life

This type of policy focuses on gaining more cash value faster, by riskier investments in equities and bonds. While more cash value sounds attractive, you're also risking losing your cash value. In some cases, the cash value that was built up for years can be wiped out in just a few months in a bad market since there is no floor. Most people avoid this type of universal life insurance.

Pros

- Offers the highest potential cash value growth.

Cons

- Aggressive investment approach that can grow, but also lose cash value significantly.

Guaranteed Universal Life

Guaranteed universal life resembles a term life insurance policy the closest. They offer little to no flexibility, and build little to no cash value. However, this policy is more affordable than other universal life options, and it still covers you for your entire life.

Pros

- Safest investment approach.

- Most affordable universal life option.

- Mimmics a term life policy, but lasts your entire life.

Cons

- Does not offer the same flexibility other universal life insurance options offer.

- Grows little to no cash value.

Our recommendation

Unless you are a seasoned investor that is looking for aggressive growth to build tax-free wealth, we recommend an indexed universal life insurance policy. It has the healthiest balance between cost, growth and flexbility.

An Indexed Universal Life (IUL) Insurance policy allows for various investments, including the S&P 500, which has shown an average annual return of 10%-11% since 1926.